Depreciation

Depreciation refers to the decline in the value of fixed assets due to their usage or passage of time. It can be defined as the non-cash expense which is the assumed wear & tear to machinery.

Being a non-cash expense it does not involve any cash outflow and is accounted in the debit side of P&L account.

There are different methods which are used by the companies to calculate depreciation.

There are different methods which are used by the companies to calculate depreciation.

Types of Depreciation Methods:

- Straight Line Depreciation Method

- Diminishing Balance Method

- Sum of year method

- Unit production method

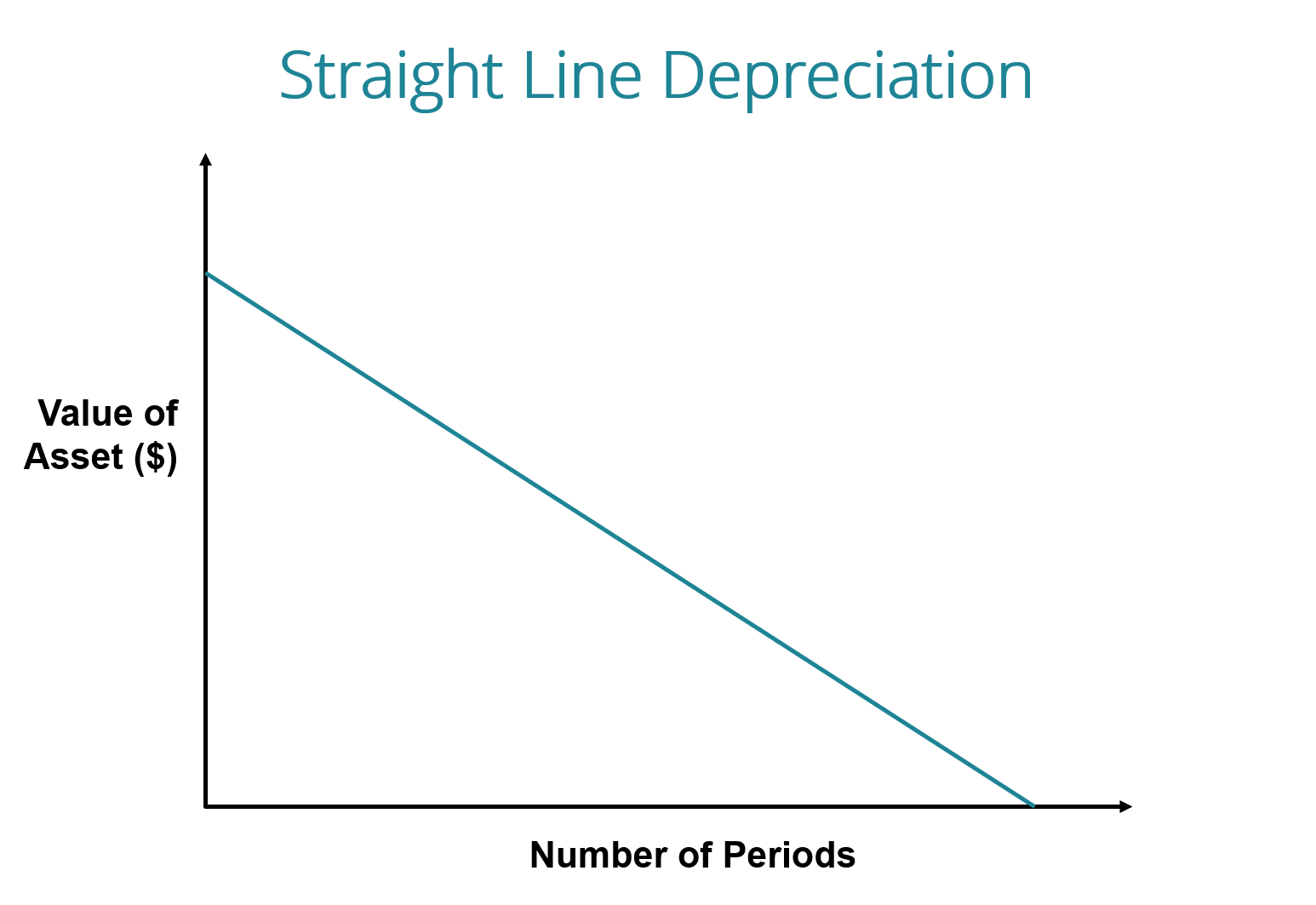

Straight Line Depreciation Method:

Under this method, the fixed asset is depreciated by the same amount every year.

With the straight-line depreciation method, the value of an asset is reduced uniformly over each period until it reaches its salvage value. Salvage Value is the residual or scrap value of the asset.

It is calculated by simply dividing the cost of an asset, less its salvage value, by the useful life of the asset.

Depreciation expense = Fixed Asset's Cost - Salvage Value

Useful Life Span of Asset

Let's take an example, a company purchases a piece of machinery for Rs. 50,000. The useful life of machinery is assumed to be 5 years by the company after which the residual value will be Rs.1000. Here's how the depreciation will be calculated by Straight Line Depreciation Method:

Depreciation expense per year = 50,000 - 1,000

5

= Rs.9800

Diminishing Balance Method:

Under this method, depreciation is charged at a fixed percentage on the asset's book value. It is also known as the Written Down Value Method or the Reducing Balance Method.

Here the rate of depreciation remains the same for every year by which the asset's value is depreciated.

Let's take an example, a company purchases a piece of machinery for Rs. 50,000. The rate of depreciation assumed by the company is 40% & the residual value after 7 years will be approx Rs. 1000. Here's how the depreciation will be calculated by Diminishing Balance Method:

Sum of Year Method:

This method is based on the assumption that the productivity of the asset decreases over time. Under this method, a fraction is computed by dividing the remaining useful life of the asset on a particular date by the sum of the year's digits.

Remaining useful

Depreciation expense = Life * Depreciable Cost

Sum of years' digit

Let's take an example, a company purchases a piece of machinery for Rs. 50,000. The useful life of machinery is assumed to be 5 years by the company. Here's how the depreciation will be calculated by Sum of Years' Depreciation Method:

Unit of Production Method:

The unit of production method most accurately measures depreciation for assets where the "wear and tear" is based on how much they have produced, such as manufacturing or processing equipment. Using the unit of the production method for this type of equipment can help a business keep track of its profits and losses more accurately.

This method results in greater deductions being taken for depreciation in years when the assets are heavily used.

Depreciation expense = Assets' Cost - Salvage Value * Units per year

Estimated production capability

Let's take an example, a company purchases a small manufacturing plant for Rs. 50,000. It is assumed that it can produce a total of 5,00,000 units. Average production of units per year is 1,00,000 units. Here's how the depreciation will be calculated by Sum of Years' Depreciation Method:

Really helpfull content..

ReplyDeleteKeep it up.

thank u so much.. :)

Delete